The world of consumer finance has on the whole been built by and around the needs of Boomers, Gen Xers and Millennials. However, Gen Z, born between 1997 and 2012, is not to be overlooked as they will make up the majority of banking consumers in the coming decades. These “digital natives” are set to become the UK’s biggest consumer cohort and will potentially wield a massive amount of financial clout.

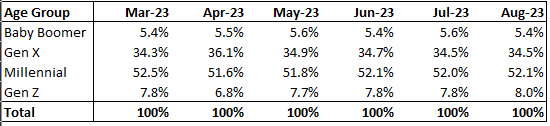

This made us think about what we could glean from our own data on this demographic and thought it would be interesting to see how the percentage of loan offers differ between the different age segments. We looked at the last six months which presented the following:

Baby Boomers: (59-77 years old)

Gen X: (43-58 years old)

Millennials: (27-42 years old)

Gen Z: (11-26 years old)

Interestingly, the percentage of Gen Z applicants that received an offer of a loan has decreased over the last 6 months, which is not the trend of the other generations.

So what does this mean? It could mean a number of things, do lenders know enough about these types of customers to make decisions on whether to make offers? What we can assume is their smaller credit footprint goes against them. This generation hasn't had the time to build up a decent sized credit file therefore lenders will see them as higher risk resulting in less offers. The tightening of criteria by lenders given the cost of living crisis is also a likely cause of offers decreasing and it’s also unlikely that many in this category will be a homeowner, another ‘tick’ when lenders come to assessing the financial health of applicants.

But are lenders missing a trick? Gen Z are already redefining digital interaction, finance and payments, and lenders can’t afford to lose out on these customers.

Research by TransUnion shows that 92% of Gen Z believe that credit monitoring is important with over half monitoring their credit score every month compared to 40% of Gen X. Surely this must give some reassurance to lenders that there is a high level of interest in becoming financially literate amongst this generation.

Gen Z are adopting new financial services and embracing digital experience (Buy Now Pay Later, open banking, richer digital banking platforms that offer greater consumer empowerment, subscription services etc.) and this reflects on the qualities they look for in businesses.

This can then flow into the potential pay-offs by investing in this demographic now and being serious about the way they are engaged with. They are early adopters of new ways of doing business, so can be seen as an extension of a ‘QA’ team helping to refine digital propositions as solutions move up the adoption curve. If businesses can begin to forge trust now and create experiences that educate and empower them, they are setting themselves up for longer-term success.

As they enter the world of further education, work and even car ownership, Gen Z becomes more invested in the search for credit. However, amongst Gen Z, research from TransUnion also shows that over 92% considered access to credit at least moderately important, but less than half (48%) felt they had sufficient access. With the current state of the market, it’s not surprising to observe 21% of all consumers planned to apply for new or refinance existing credit in the next year. That demand was more apparent amongst Millennial (29%) and Gen Z (40%) consumers who intended to apply, while Baby Boomers sat at just 9%.

So how can lenders build their businesses to better serve this generation and gain new customers in the process? They can:

-

Gain a better understanding of Gen Z and their needs and wants

-

Understand how they are influencing technology and how to build better digital customer journeys

-

Create opportunities to engage with them and also support them during these challenging times

-

Recognise the value of Gen Z as long-term customers

Partnerships between lenders and fintechs could help strategically reach Gen Z by leveraging the best qualities from each to create more innovative offers and services for customers. These early adopters are essentially helping to refine new financial applications and solutions as they become more widely adopted.

Fundamentally, lenders must be able to keep up with this tech savvy generation as they have the ability to make or break businesses - we should not underestimate their value now or in the future.

6-month Update:

We have been keeping an eye on the loan application trends of different age cohorts for the past six months, and we have some interesting findings to share. Our data shows that while the percentage of loan offers to Baby Boomers, Gen Xers, and Millennials has remained stable, the percentage of loan offers to Gen Z applicants continued to decline over the next three months, with the last two seeing a slight increase but not returning to 2022 levels. This trend is concerning, and it suggests that lenders are still not fully catering to the needs of these digital natives. As we highlighted in our previous post, Gen Z is a significant consumer cohort set to become the UK’s largest demographic in the coming decades. Therefore, lenders must understand this group's unique needs and create innovative digital solutions to meet their requirements.

-listing.jpg)